How serious is oil crisis?

Looking at the new all-time highs across major equity benchmarks, especially in Asia, one might conclude that we are in the midst of a strong bull market and that the oil price shock remains negligible. At the same time, oil prices remains quite elevated, while there is still no clear resolution to the situation around the Strait of Hormuz. Investors remain optimistic believers in the all-mighty Donald Trump, while the massive AI trend continues to ignite share prices across the entire AI value chain.

However, do current market valuations fully price in the inflationary pressure already being created by elevated oil prices and the extremely rapid depletion of reserves? The Strait of Hormuz is the critical artery of global energy markets. Roughly 20% of global oil supply and a significant share of LNG exports pass through this narrow corridor, with around 80% of these flows destined for Asia. While alternative routes exist, they can offset only part of the disruption. Saudi and UAE pipelines, for example, can mitigate only around 10% of global supply losses.

What makes the current episode unusual is speed. The oil market moved from oversupply to shortage within weeks. Prior to the February 2026 end, inventories were building and prices softening. The system initially absorbed the shock through strategic reserves and inventories, but those buffers are finite. After ~2 months of disruption, commercial inventories, particularly in Europe and Asia, have been drawn down materially, reducing the system’s ability to cushion further shocks. JP Morgan warn inventories are reaching the minimum operational level. The US has one of the biggest inventories, but gasoline and distillate are dropping rapidly. Even oil at sea is declining. So as inventories and oil at sea run out, the actual shortage could double from 4 million a day to up to 8 million a day (link). Importantly, even if the strait reopens, physical normalization lags: it takes 2–4 weeks for oil cargoes to reach Asian markets, meaning supply tightness persists beyond the headline event.

Why are markets not alerted?

Primarly, because the whole AI value chain, starting with energy infrastracture, and electricity companies and ending with hyperscallers distributing AI solutions to end users, demonstates robust figures, driving S&P EPS growth projections. According to Bloomberg, S&P 500 earnings growth in 2026 set to be the highest since 2021, to a large extent driven by AI development.

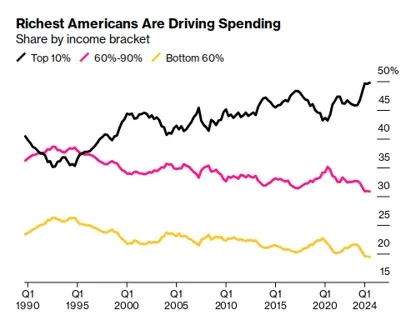

In addition, economies globally are becoming increasingly polarized, with a relatively small number of households driving the majority of consumption. In the US, for example, the top 10% income bracket accounts for roughly 50% of total spending. Given the resilience of wealthier households, a collapse in aggregate consumer spending is not widely expected, despite the spillover effects of higher oil prices on broader inflation and other product categories.

Worst case scenario

A sustained oil shock hits equities through two measurable channels: margins and multiples. On margins, energy and freight costs rise immediately while pricing lags. In past spikes, fuel and logistics can move 20–50% in months, while most companies reprice quarterly at best. Sectors like airlines, chemicals, packaging, and transport typically see 200–500bps margin compression if oil stays elevated. Particularly vulnerable are companies with structurally lower margins and limited pricing power, as they struggle to pass rising costs on to consumers. The consumer discretionary sector could be among the hardest hit, given its negative exposure to inflationary environments and weakening purchasing power.

At the same time, higher inflation forces central banks to hold or raise rates, pushing real yields up and compressing valuations (e.g., a +100bps move in real rates can take ~10–20% off equity multiples). The worst case is therefore mechanical: EPS down 10–20% + multiples down 10–20% = 20–40% equity downside, even without a financial crisis.

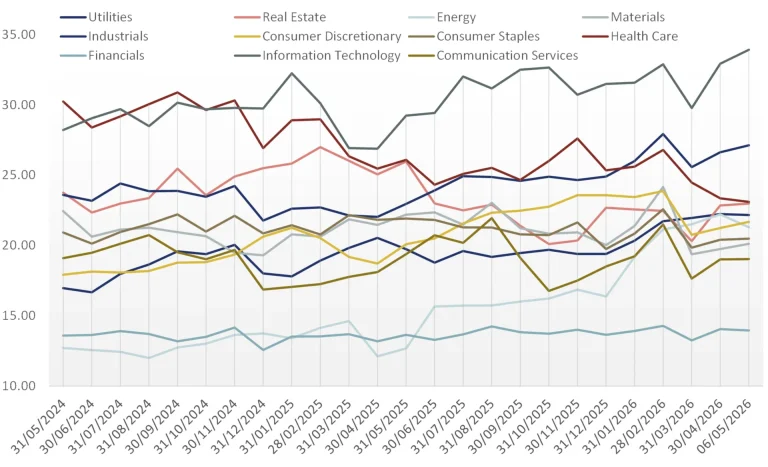

Considering multiples development, one sees PE level in the majority of sectors are close to the levels we saw before the US-Iran conflict with IT sector exceeding the level. The sector with clearly lower multiples are Communications, Health care and Materials.

Overall, markets may have rational reasons for optimism, particularly due to strong AI-driven earnings growth and resilient consumer spending, but current valuations appear to underestimate the risks of a prolonged oil supply shock and renewed inflationary pressure. If energy disruptions persist and inventories continue to tighten, today’s market optimism could ultimately prove to be less a true reflection of fundamentals and more of a “Don’t Look Up” moment.

Implications for Quality investing

In this regime, screening for quality shifts toward gross margin stability, pricing frequency, and energy intensity. The winners are those that can defend cash flow within 1–2 quarters of a cost shock. The companies with strong pricing power, and the companies with strong global trends behind, and, above all, strong fundamentals should be a good combo in this market environment.

ADVERTISEMENT

This document has been prepared solely for information and advertising purposes and does not constitute a solicitation offer or recommendation to buy or sell any investment product or to engage in any other transactions.