It only takes a few

What does a uniform rental company have in common with a manufacturer of advanced power electronic solutions? Both – Cintas and Monolithic Power Systems – have been amongst the most consistent compounders of the last decade, outperforming each year. Finding just a few winners like these and holding on to them magnifies your portfolio return exponentially, especially if you are concentrated in a handful of high conviction ideas: over the past 90 years, just 86 stocks have accounted for half of the stock market value creation in the US1. We know – easier said than done –, but there are a few common patterns that emerge when studying the winners of the last 10 years, which we are diving into in this article.

High performers are scarce

To set the stage, we are looking at the companies in the MSCI World Index that have managed to deliver a 10-year (31/03/2014-31/03/2024) total return (in local currencies) above sample average and compare them to the trailing cohort. For comparability purposes we only include companies that have been listed for all 10 years. The good news is, if you had invested in a random stock (highly unadvisable) 10 years ago, chances are you made some money. Only 16% out of 1778 companies in our sample delivered negative returns against 254% average gain. The bad news is, outperforming is harder, as only 28% performed above average. Even amongst the winners, dispersion of returns is substantial. On average, the winners have a compounded 20% annualized rate, but the top 10 performers have delivered 52% CAGR.

Winners keep winning

Looking at the consistency of outperformance of long-term winners (Fig. 1), only a few companies have demonstrated consistent market-beating performances year after year throughout the entire 10-year period. This stresses the importance of taking a long-term view – even the best companies can face temporary headwinds. At times, there may not even be any issues the business is dealing with, but the market just rotates into a different style or sector, as was the case in 2022. Still, outperformance of winners is usually not the result of a couple of blast years: long-term compounders deliver above-market returns more often than not, while underperformers tend to consistently disappoint. Therefore, you are likely to make more money buying a great company at a fair price, rather than buying a troubled business trading cheap, hoping that the worst is priced in, and a turnaround is near.

Figure 1: Sample distribution by the number of years in which companies outperformed

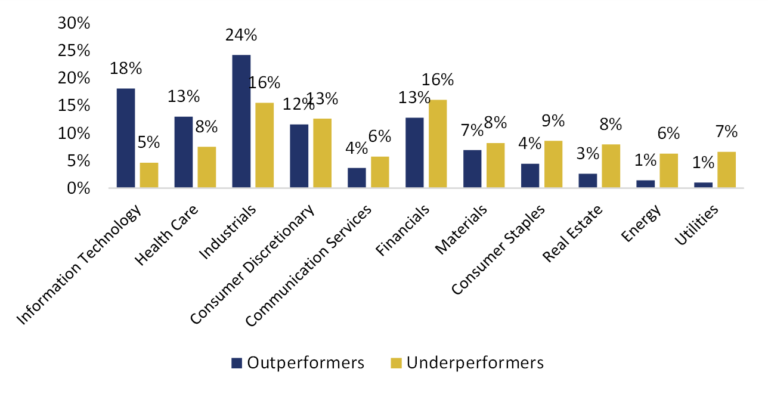

Going with the trend

Looking at the sectoral structure of winners versus losers, three sectors emerge as frontrunners in producing top performers – IT, Health Care and Industrials (Fig. 2).

Figure 2: Sample distribution by sector

Among the top 20 performers, 13 were semiconductor-related titles. Nvidia has certainly led the pack with >20,000% total return, but there were plenty of lower-profile names with stellar return, such as Lasertec (>16,000%), Disco (>3,000%), Advantest (>2,000%), Tokyo Electron (>2,000%) and Cadence (>1,900%). This shows that winners are more likely to come from areas of the economy that are supported by multi-year secular growth trends. For example, in the coming years, AI, Robotics, Reshoring and Electrification are some of the areas that are likely to gain traction. At the same time, presence of winners in virtually all sectors also suggests that there are no inherently ‘good’ or ‘bad’ places to invest in, and a great portion of success rests upon the companies’ prowess.

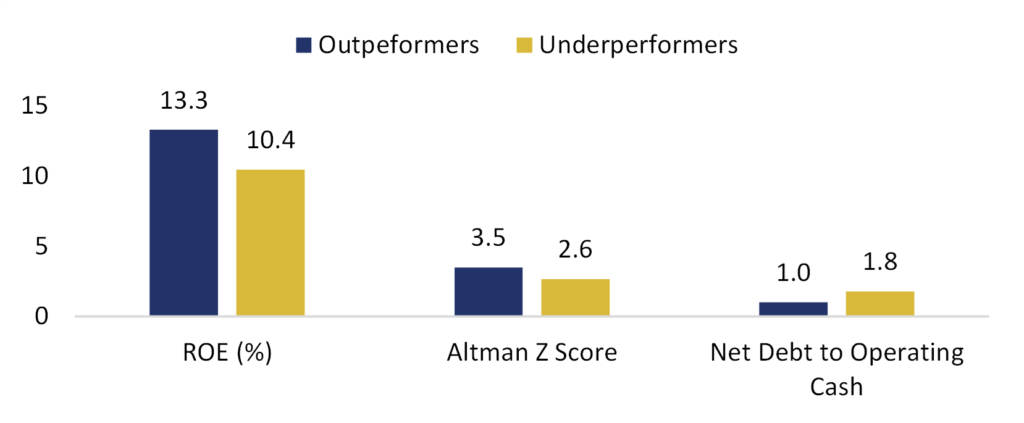

A solid foundation to begin with

Still, however supportive the macro backdrop is, the quality of the business should come first when investing for the long term. The best investments of the last decade, on average, exhibited higher ROE, lower leverage and better financial stability already at the beginning of the analysis period (Fig. 3). While there are always exceptions to the rule, this highlights the importance of paying attention to the financial health of investment candidates.

Figure 3: Financial characteristics of outperformers and underperformers at the beginning of the analysis period (median)

What about valuation?

As it seems, price multiples play little role in determining which companies will prove to be great investments. Looking at the starting median P/E ratio of companies that went on to outperform, it was even higher compared to the laggards (Fig. 4). Furthermore, over time the P/E of these companies has expanded, while the median multiple in the bottom cohort has contracted. Having said that, a comparison of share price and EPS growth rates clearly suggests that P/E expansion played only a minor role in total return.

Figure 4: Price multiples of outperformers and underperformers (median)

The winning formula

So, what do Cintas, Monolithic Power Systems and other high performers have in common? Quality is where these different business models often meet. Of course, companies not considered quality in the traditional sense can also rise to the top. We would have never guessed that the best-performing company in our sample would be Pilbara Minerals, an Australian lithium miner. However, looking at the top 100 performers – many names are familiar to us. Of them, 71% are a part of our quality cluster (excluding companies not in our universe). The next decade will bring a new set of winners, but we think that the quality investment universe is a good starting point for the search of future compounders.

References

- Bessembinder H. (2018). Do stocks outperform Treasury bills?

ADVERTISEMENT

This document has been prepared solely for information and advertising purposes and does not constitute a solicitation offer or recommendation to buy or sell any investment product or to engage in any other transactions.