Quality momentum

Global equity markets have continued their strong performance this year, supported by rising earnings expectations. While much of this earnings growth remains concentrated in the technology sector, the broader trend has been one of improving corporate fundamentals. Following the earnings setback in 2022, expectations have steadily recovered since 2023, and their acceleration has been a major driver of market returns, highlighting the importance of fundamental momentum.

Figure 1. S&P 500 Earnings Expectations development

Improving financial performance may now be becoming more important than a company’s already-established quality characteristics. This represents a notable shift from traditional quality investing. The upside potential of many high-quality companies is often constrained by elevated valuations, as broad and immediate access to information enables investors to quickly identify and price business quality. In contrast, companies experiencing accelerating earnings growth, expanding cash flows, improving margins, or rising returns on invested capital often outperform because markets react more strongly to positive revisions in expectations than to already-recognized quality.

Academic research increasingly supports this view. Studies show that fundamental momentum, particularly earnings momentum, explains a significant share of traditional price momentum returns and continues to generate excess returns even after controlling for price momentum effects (Novy-Marx, R., 2015; Ma, T., Sheng, H. & Wang, Y., 2024).

As quality investors, we focus primarily on companies with strong fundamentals, which are often evidence of durable competitive advantages. However, we increasingly incorporate a growth dimension, emphasizing earnings revisions, accelerating business performance, and exposure to structural growth trends. This raises an important question: can the highest-quality companies continue to grow faster than the market, or does exceptional quality eventually become a constraint on future growth?

Fundamental Momentum of Corporate Excellence

Our Corporate Excellence Award initiative can be described as a form of “beauty contest” for listed companies globally. Its goal is to recognize top-quality companies worldwide by evaluating both quantitative fundamentals and qualitative characteristics such as economic moat, strong governance (interpreted as the long-term consequence of financial discipline), and the overall strength and resilience of the industry in which a company operates. The framework emphasizes the static picture of corporate quality, while initially giving less weight to the dynamics of financial change.

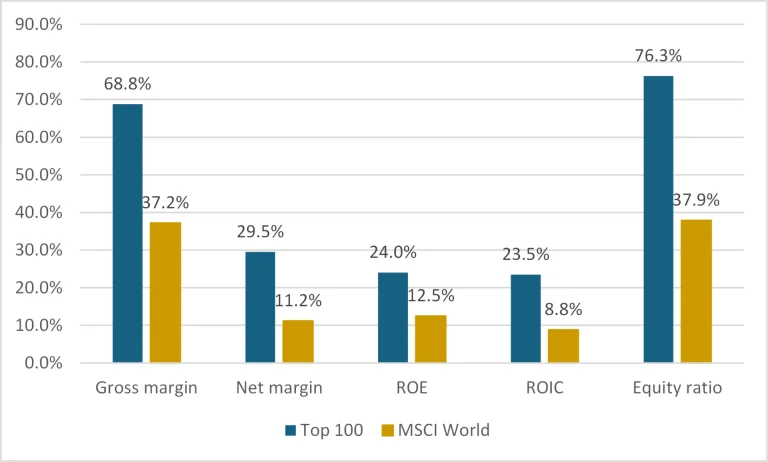

Figure 2 illustrates a clear difference in current fundamental characteristics between the Top 100 companies and the MSCI World AC constituents. There is a substantial gap in profitability and balance sheet strength. The key question now is whether this already elevated level of quality can be improved further over time.

Figure 2. Financial characteristics of Top 100 vs. MSCI World in 2025

Reality check: room for growth possible?

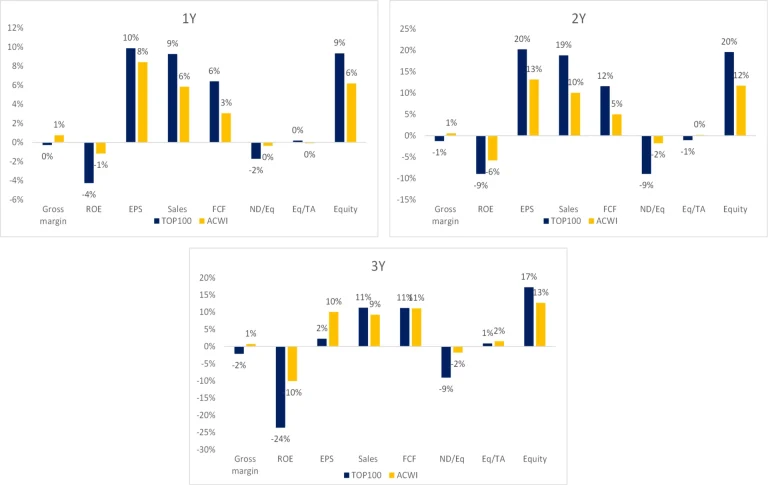

Our analysis compares the financial development of the Top 100 companies selected under the Corporate Excellence Award methodology with the broader MSCI ACWI universe over the past three years.

The results suggest that high-quality companies continue to deliver above-average growth despite their already strong starting position. Revenue, free cash flow, and earnings-per-share growth have generally exceeded those of the broader market. This indicates that quality does not necessarily come at the expense of growth. However, profitability margins did not improve further. On average, gross margins among the Top 100 companies declined by 1–2%, while the broader market recorded modest margin expansion. This suggests that sustaining exceptionally high profitability levels may be more challenging than growing revenues and earnings.

Fig.3. Dynamics of financial ratios for Corporate excellence top 100 selections in 2023, 2024, 2025 (1Y: 2025; 2Y: 2024-2025; 3Y: 2023-2025)

Both the Top 100 companies and the broader market experienced declines in capital profitability ratios. A key reason appears to be the accumulation of equity capital and balance-sheet strengthening. This interpretation is supported by declining net debt-to-equity ratios, with the Top 100 companies improving their balance sheets faster than the market as a whole.

The evidence suggests that quality and growth are not mutually exclusive. Although the highest-quality firms appear to have limited room for additional margin expansion, they continue to strengthen their balance sheets and deliver above-average growth. This indicates that quality can serve not as a barrier to growth, but as a foundation that enables companies to sustain superior performance over time. Consequently, combining quality with improving fundamentals and positive earnings momentum may offer a more effective framework for identifying future market leaders than focusing on quality alone.

References

Ma, T., Sheng, H., & Wang, Y. (2024). Noisy market, machine learning and fundamental momentum. Pacific-Basin Finance Journal, 86, 102473.

Novy-Marx, R. (2015). Fundamentally, momentum is fundamental momentum (No. w20984). National Bureau of Economic Research.

ADVERTISEMENT

This document has been prepared solely for information and advertising purposes and does not constitute a solicitation offer or recommendation to buy or sell any investment product or to engage in any other transactions.