ESG Backlash and Market Repositioning

Over the past two years, financial markets have seen a strong backlash against ESG and sustainability trends, accelerated by the election of Donald Trump and a shift toward more conservative economic policies. Many Wall Street institutions have scaled back Diversity, Equity and Inclusion initiatives and other sustainability-related practices.

Figure 1. US companies abandoning DEI policies

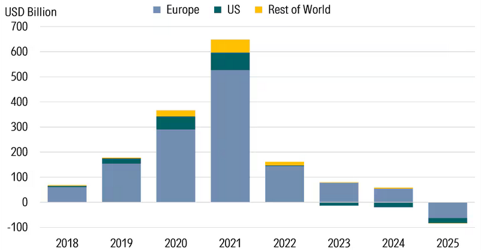

In Europe, Omnibus regulation aims to ease ESG reporting requirements to protect competitiveness in a more challenging geopolitical environment. This shift is clearly reflected in fund flows. According to Morningstar (fig. 2), ESG inflows have declined significantly since 2021, with 2025 marking net outflows in Europe (for the first time) and continued outflows in the US (third consecutive year). ESG ETFs remain under pressure, as investors face intangible, long-term outcomes, mixed performance, reduced regulatory support, and geopolitical uncertainty.

Figure 2. Annual global sustainable fund flows

ESG may have become overregulated and overmarketed, encouraging greenwashing rather than real impact. However, now, possibly it could be the perfect time to look back into the sustainability topic, which has enjoyed good returns last year, while also leaving room for future growth.

With oil supply chain fragility and multiple bottle-necks, the talks of sustainability are resuming in order to make businesses more resilient and free from fossil fuel dependence. Can the current situation stimulate more investments into sustainability and efficiency?

Favourable Megatrends and Structural Mismatch

Sustainability, efficiency, and electrification remain powerful megatrends supporting industrial growth. In a world of intense competition, cost efficiency is becoming a decisive factor, and industrial companies play a key role by providing technologies and equipment that enable businesses to improve productivity and reduce emissions.

In fact, industrial players are the primary enablers of the transition toward greener economies and a higher share of net-zero companies. However, there is an interesting mismatch: sustainability and climate indices—such as those constructed by MSCI—are often heavily weighted toward technology, financial and healthcare sectors, while industrials tend to be underrepresented. For example, MSCI World Climate Transition has 31% exposure to tech and 15% to financials, while MSCI ACWI SDG Impact index has 21% exposure to health care and 18% – to IT. By contrast, portfolios with a stronger exposure to industrial companies can offer more direct participation in the sustainability transition. These companies typically generate a higher share of “green revenues” and are well positioned to benefit from efficiency-driven demand that is increasingly supported by business needs rather than regulation alone. For instance, average share of ‘green revenues’ at OHOR sustainable quality portfolio is 34%.

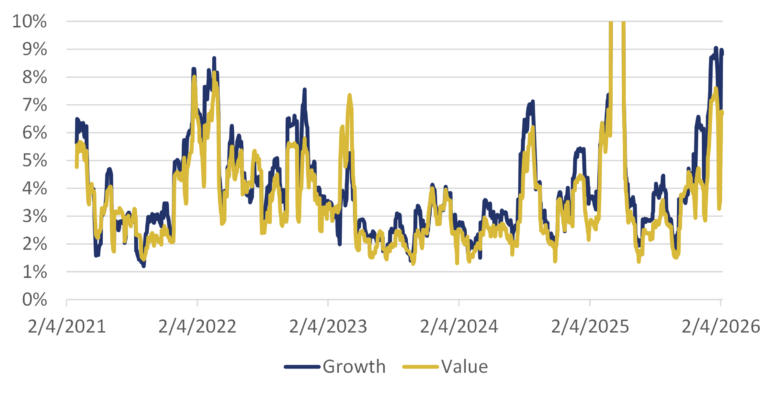

Another Supporting Trend: Capex and Infrastructure

Until the recent oil price shock, declining interest rates were one of the main drivers of industrial capital expenditure. This environment was particularly supportive after several years of underinvestment (fig. 3).

Figure 3. New order book at US Manufacturers, 1992-2026

In addition, aging infrastructure provides further support for investment flows into the sector. For example, Germany has launched a €500 billion investment program focused on infrastructure and climate neutrality. UK commits over £725 billion to modernize infrastructure till 2035. Similarly, the United States faces a substantial need to modernize its power grid.

At the same time, hyperscalers are sitting on large cash reserves and are directing significant investments toward infrastructure build-up, driven by AI-related demand. According to consensus estimates linked to the S&P 500, earnings growth is expected to reach around 15% in 2026. However, geopolitical risks—such as tensions affecting oil markets—may lead to higher energy prices and inflation, potentially slowing down capex plans.

Quality layer on top of global trends

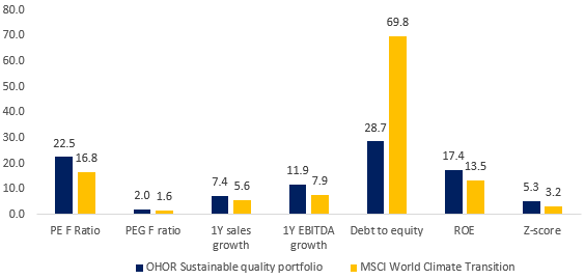

Combining sustainability exposure with strong corporate quality characteristics can significantly improve portfolio robustness. High-quality companies tend to offer better financial stability while maintaining strong growth and profitability (fig. 4). In average OHOR sustainable quality portfolio firms managed to grow revenues by 7.4% and EBITDA – by 12% as compared to the MSCI World Climate Transition constituents growing by 5.6% and 7.9% respectively. Financial solidity is substantially stronger in case of quality firms: debt to equity ratio is 29% vs. 70% and Altman 5.3 vs. 3.2. Quality firms also boast of stronger capital profitability: 17.4% vs. 13.5%. While valuation multiples for higher-quality companies are typically elevated, the premium appears justified.

Figure 4. Financial and valuation ratios of OHOR sustainable quality portfolio and MSCI Climate Transition

So, the bottom line: The shift from regulation-driven to economically driven sustainability is key. Industrial companies, supported by infrastructure spending and AI-related demand, are likely to be central beneficiaries. Their development might be a bit volatile in case of rate increase, but in this case sustainable strategies with a strong quality focus offer a balanced approach—combining resilience with exposure to long-term growth.

ADVERTISEMENT

This document has been prepared solely for information and advertising purposes and does not constitute a solicitation offer or recommendation to buy or sell any investment product or to engage in any other transactions.